随着健康消费理念深化,能量饮料应用场景加速延伸,形成以工作学习提效为核心的功能需求圈层,以运动健身、长途驾驶为延伸的活力补给场景,以及依托口味创新与包装迭代驱动的年轻消费生态。根据全球领先的新经济产业第三方数据挖掘和分析机构iiMedia Research(艾媒咨询)最新发布的《2025年中国能量饮料行业发展状况与消费行为调查数据》数据显示,消费者消费频率呈现规律化特征,41.25%消费者每周饮用1-2次。工作/学习场景以31.21%占比位居消费动因首位,功能性诉求显著。市场格局呈现典型头部效应,红牛以46.54%市占率稳居榜首,罐装包装以38.81%偏好度成为主流载体。

44.10%消费者接受7-8元价格带,42.47%首选250-400ml规格,41.66%将口味作为核心选购标准。渠道选择呈现双轨特征,综合电商平台和线下小型零售终端各有优势。行业升级面临双重挑战:36.91%消费者期待价格优化,36.09%关注功效提升,反映性价比与产品力协同不足。买一送一促销形式以39.62%偏好度彰显价格敏感特征。艾媒咨询分析师认为,企业应构建功能强化+体验升级双维竞争力:一方面开发7-9元黄金价格带专属产品,强化250-500ml规格矩阵;另一方面深化电商渠道大数据应用,针对不同消费者创新不同品类。(《艾媒咨询 |2025年中国能量饮料行业发展状况与消费行为调查数据》完整高清PDF版共40页,可点击文章底部报告下载按钮进行报告下载)

With the deepening of the concept of healthy consumption, the application scenarios of energy drinks accelerate the extension, forming a functional demand circle with the efficiency of work and study as the core, a vitality supply scene with sports fitness and long-distance driving as the extension, and a young consumer ecology driven by taste innovation and packaging iteration。 According to the latest “China energy drink industry status and consumption behavior survey data in 2025” released by iiMedia Research, the world’s leading third-party data mining and analysis organization for the new economy industry Consumption frequency showed regular characteristics, 41。

25% of consumers drank once or twice a week, work/study scene accounted for 31。21% of consumption motivation, functional appeal was significant。 The market pattern presents a typical head effect, with Red Bull ranking first with a market share of 46。54%, and canned packaging becoming the mainstream carrier with a preference of 38。81%。

44。10% of consumers accept the 7-8 yuan price band, 42。47% prefer 250-400ml specifications, 41。66% will taste as the core selection criteria。 Channel selection presents dual-track characteristics, and both integrated e-commerce platforms and offline small retail terminals have their own advantages。 Industry upgrading faces dual challenges: 36。91% of consumers expect price optimization, 36。09% pay attention to efficiency improvement, reflecting the lack of coordination between cost performance and product power。

The form of buy one get one free promotion shows the price-sensitive characteristics with 39。62% preference。 iiMedia Research believe that enterprises should build function enhancement + experience upgrade dual-dimensional competitiveness: on the one hand, develop 7-9 yuan gold price belt exclusive products, strengthen 250-500ml specification matrix; On the other hand, deepen the application of big data in e-commerce channels and innovate different categories for different consumers。(“iiMedia Report |China energy drink industry status and consumption behavior survey data in 2025” full version has 40pages, please click the download button at the bottom of the article to download the report)

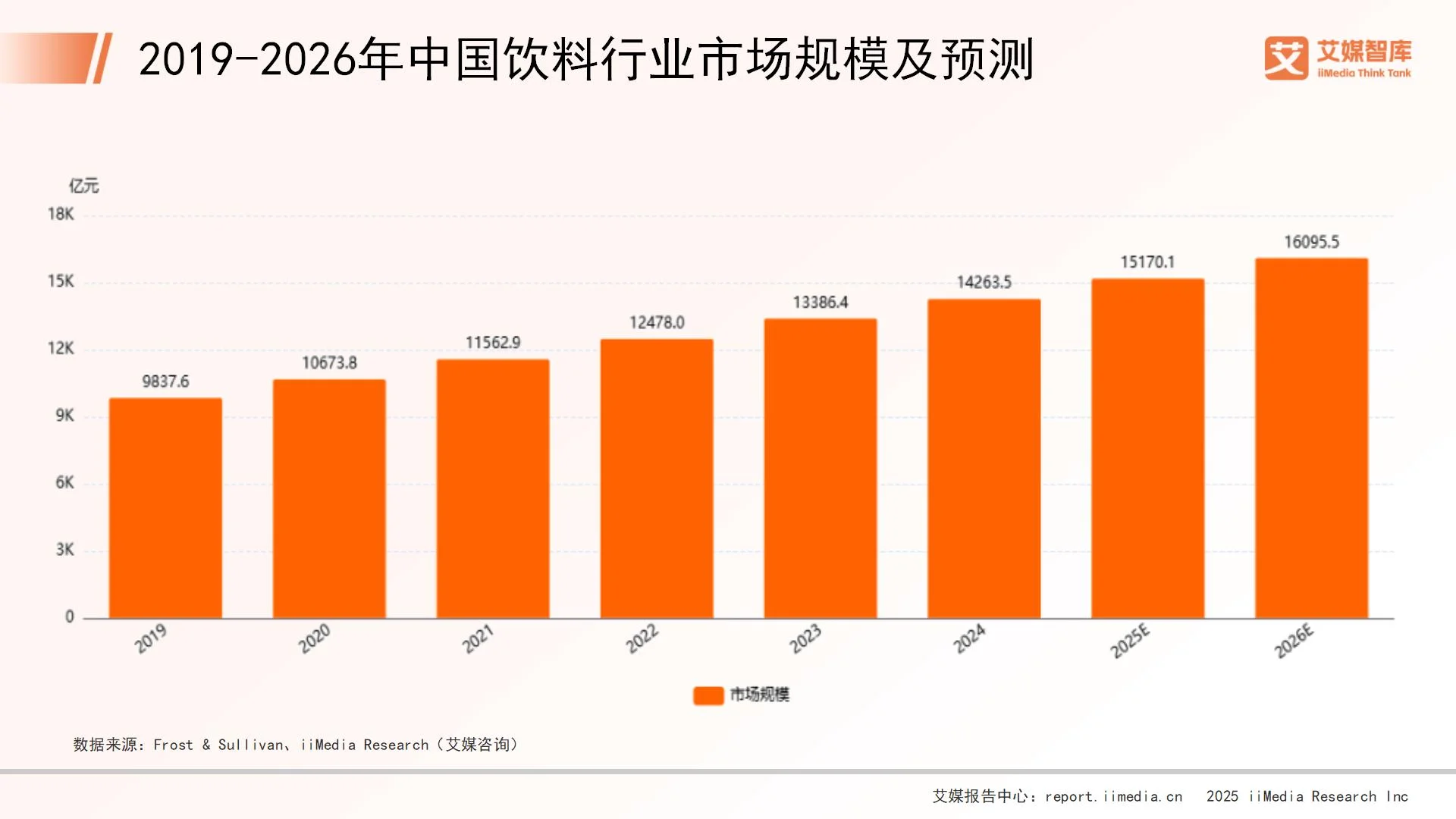

2019-2026年中国饮料行业市场规模及预测

数据显示,在2019到2026年间,中国饮料行业的市场规模呈现上升趋势,2024年达到14263.5亿元,比2019年增加了4425.9亿元,增长了44.99%。这说明中国饮料行业发展迅速,规模在不断扩大。预计2025年市场规模可达15170.1亿元,2026年可达16095.5亿元。

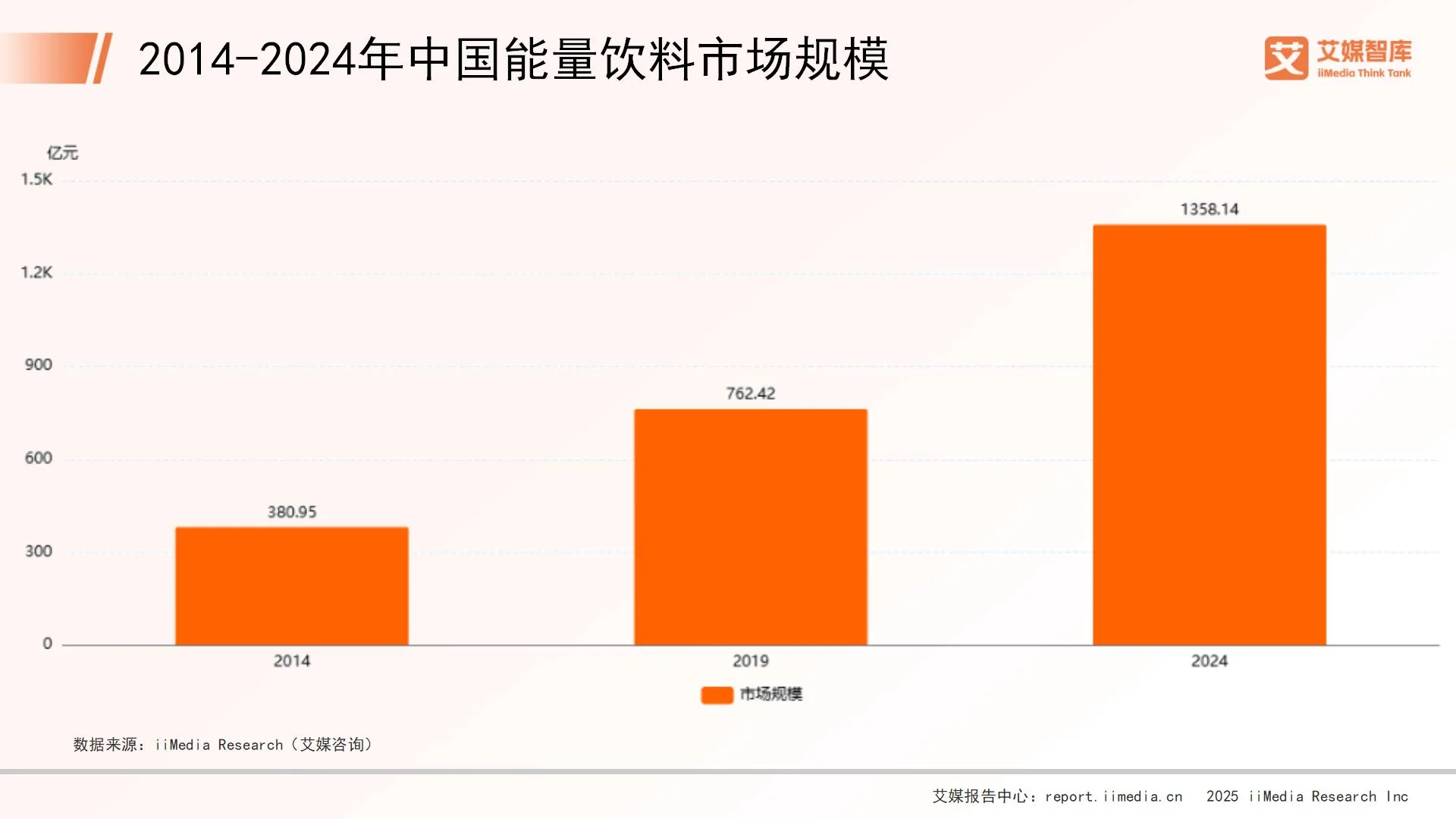

2014-2024年中国能量饮料市场规模

数据显示,在2014到2024年间,中国的能量饮料市场规模总体呈现上升趋势,2024年市场规模达1358.14亿元,比起2014年增加了977.19亿元,增长了257%。这说明近十年间中国能量饮料的需求量在不断增加,中国能量饮料的市场潜力巨大。

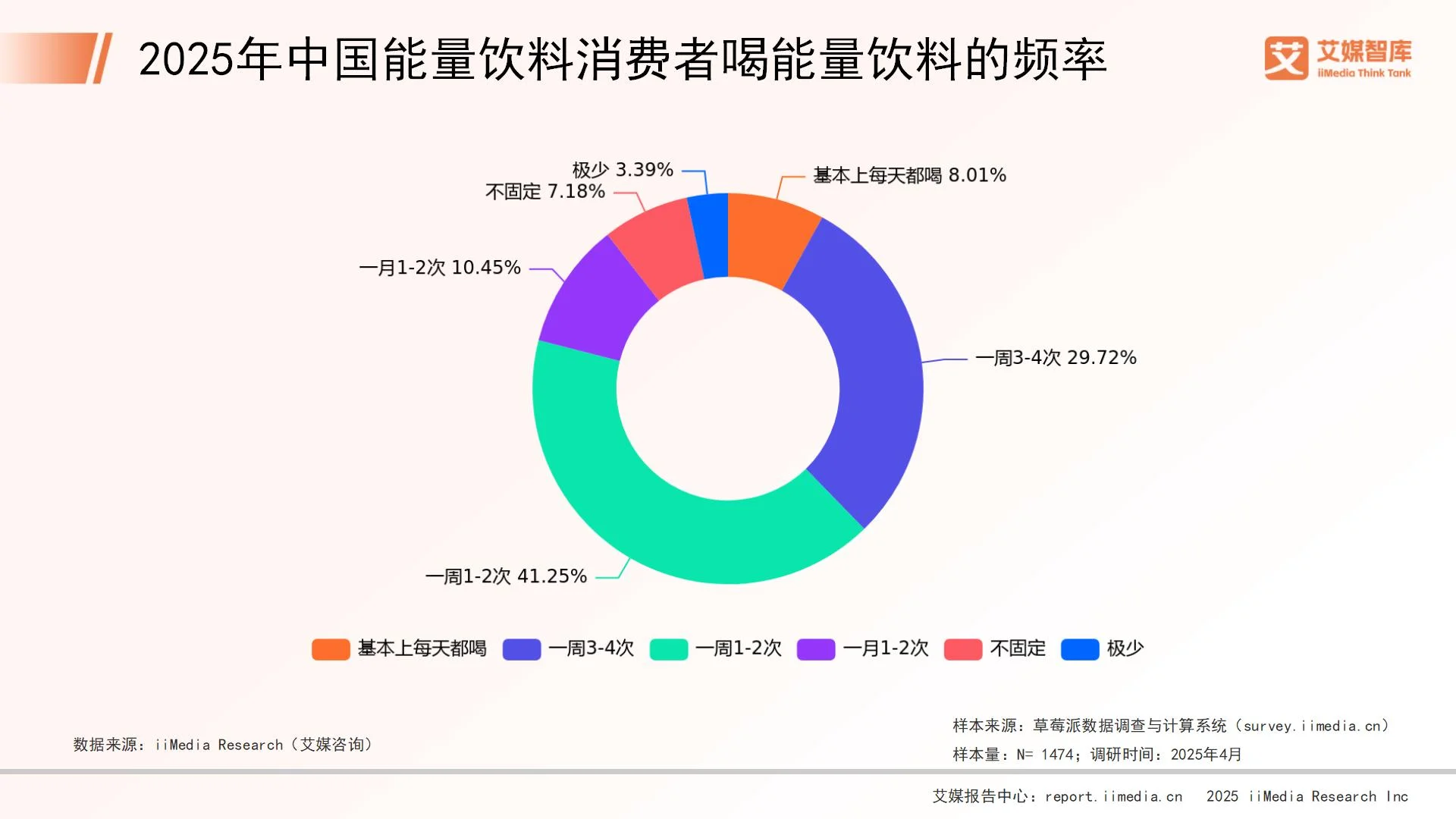

2025年中国能量饮料消费者喝能量饮料的频率

数据显示,在2025年中国能量饮料消费者中十大品牌网,一周1-2次的频率最高,占比41.25%。其次是一周3-4次,占比29.72%。一月1-2次的消费者占比10.45%,基本上每天都喝的消费者占比8.01%。不固定和极少的消费者占比分别为7.18%和3.39%。总体来看,大多数消费者选择每周1-2次或3-4次饮用能量饮料,每天饮用和极少饮用的比例较低。

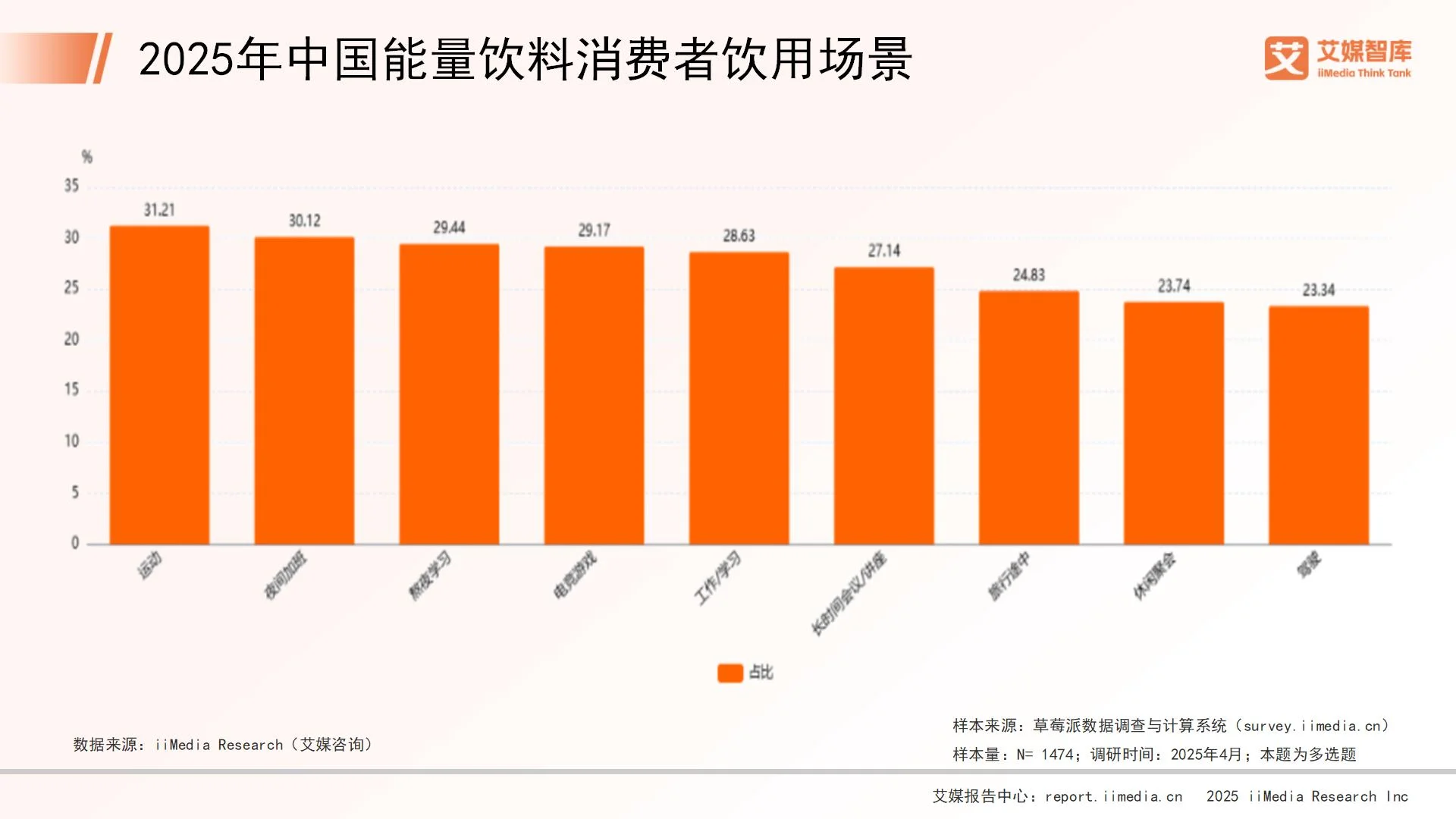

2025年中国能量饮料消费者饮用场景

数据显示,在2025年中国能量饮料消费者饮用场景中,运动场景的占比为31.21%,位居第一,说明能量饮料在运动人群中有很大需求。其次是夜间加班与熬夜学习场景,分别占比30.12%和29.44%,表明能量饮料在夜间应对疲劳,提升工作学习效率方面有较大需求。电竞游戏场景占比29.17%,其他饮用场景的占比均低于29%,其中驾驶场景的占比最低,为23.34%,可能是因为驾驶时不宜摄入过多能量饮料,以免影响驾驶安全。

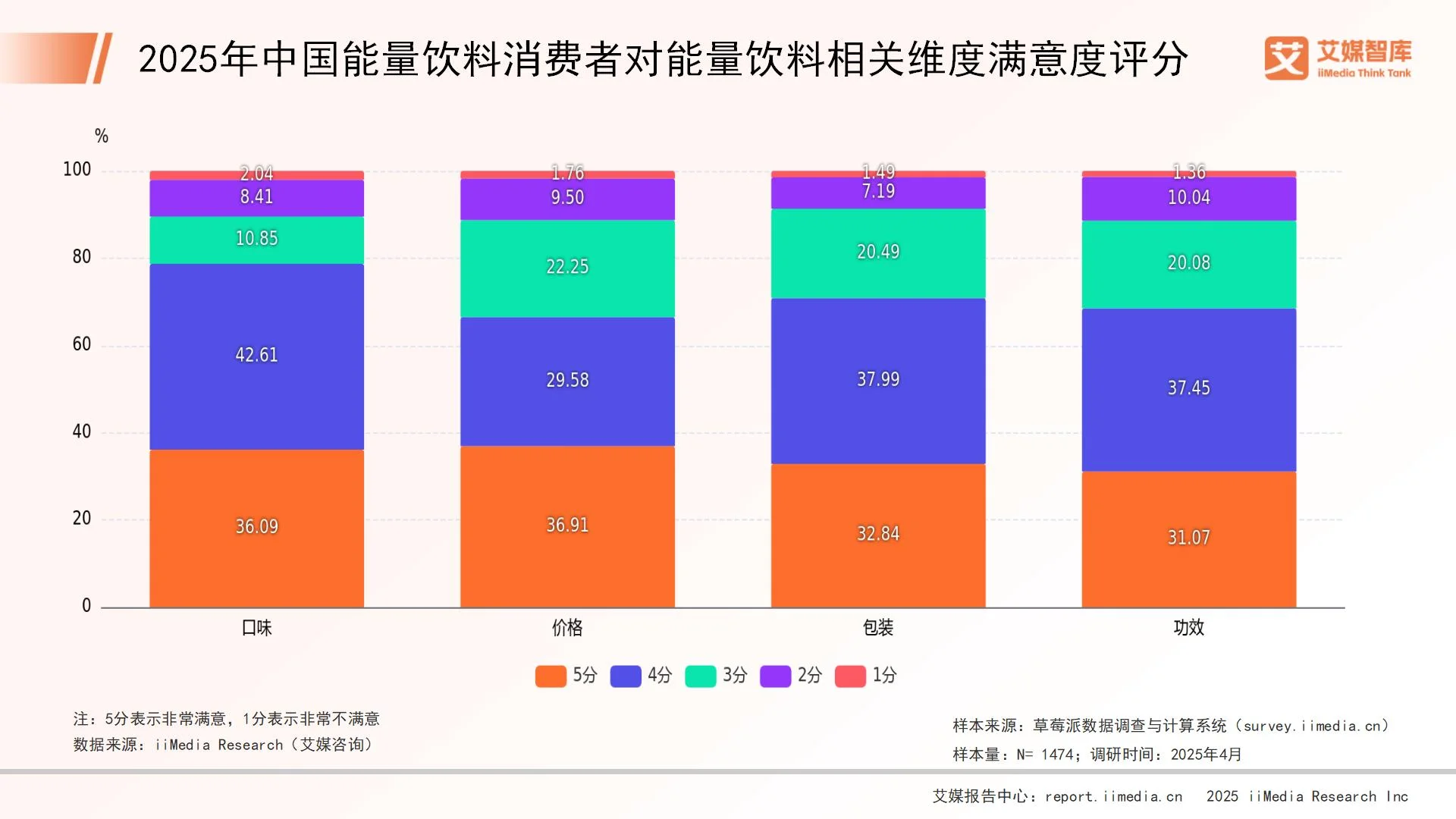

2025年中国能量饮料消费者对能量饮料相关维度满意度评分

数据显示,在2025年中国能量饮料消费者满意度评分中,价位维度获得最高满意度,其中5分评分占比为36.91%,显示出消费者对能量饮料价格的高度认可。其次是口味维度,5分评分占比为36.09%。包装维度的满意度相对较低,5分评分占比为32.84%。功效维度的满意度最低,5分评分占比为31.07%。

微信扫一扫打赏

微信扫一扫打赏